Becoming an employer: what you need to know

Welcome to “employerhood”!

Taking on your first employee is a huge milestone for you and your business. In the UK, any kind of business can employ people: sole traders and partnerships can employ anyone except their business owners, while limited companies can employ their directors as well as other individuals.

There are a whole host of different things you need to think about when you become an employer. Among other responsibilities, you’ll have to comply with tax legislation and employment law, and report to HMRC how much you pay your staff and deduct from their salary. In this guide, we outline the key procedures that you’ll need to follow to ensure a smooth transition into employerhood.

Registering as an employer

Unless you're going to pay all your employees less than the Lower Earnings Limit for National Insurance (£123 per week), you must register as an employer with HMRC before you take on any members of staff. If your business is a limited company and you’re taking a salary, you may well have already registered the company as an employer. If this is the case, you won’t need to register again when you take on your first employee.

Salary and non-cash benefits

Another vital step is to decide how much to pay your new employee; as a minimum, you must pay the National Minimum Wage (NMW) to employees under 23 years of age and the National Living Wage (NLW) to employees aged 23 and above. You should also decide how often to pay your new member of staff. Weekly and monthly payment are both popular options among employers but there are no hard and fast rules - it’s up to you to decide what’s best for your business.

Current National Minimum Wage and National Living Wage rates

| Apprentice | Under 18 | 18 to 20 | 21 and over (NLW) |

|---|---|---|---|

| £6.40 | £6.40 | £8.60 | £11.44 |

You may want to consider supplementing the employee’s salary with some non-cash benefits, such as childcare or the Cycle to Work scheme. If you decide to offer non-cash benefits in exchange for a reduction in salary, you’ll need to make sure you comply with the rules for salary sacrifice. You will also need to file a form P11D by 6th July each year to declare any non-cash benefits you provided in the previous tax year.

Employer’s National Insurance

Employer's National Insurance is calculated at 13.8% of the amount an employee earns over and above the Secondary Threshold of £758 per month (£9,096 per year).

Source: HMRC

You won’t have to pay employer’s National Insurance on the wages of any staff members who are under 21, unless you pay them more than £967 a week.

You may be able to reduce your employer’s National Insurance bill through the Employment Allowance, which reduces the amount of employer’s National Insurance for nearly all employers.

Employment Law (in association with LawBite)

![]()

Essential dos and don’ts for first-time employers

As a new employer, there are a number of requirements you must meet from an employment law perspective. Here are some of the key dos and don’ts:

Dos

- Check that the candidates you consider for the role have the right to work in the UK.

- Carry out any other checks that are necessary for the role (e.g. criminal record checks for jobs that involve working with children or vulnerable adults).

- Familiarise yourself with employees’ rights to holiday and sick pay in the UK and decide what to offer your employee in both these regards.

- Prepare either a statement of terms and conditions or a contract of employment (see below for more information).

- Remember that once the employee starts, you have a responsibility to provide a safe and secure working environment.

Don'ts

- Don’t ask candidates any questions about their health during the interview process. When you make an offer, you may only ask the successful candidate questions about their health that are relevant to the job.

- Don’t write any notes about a candidate that you wouldn’t want to share in a court or tribunal.

- Don’t forget to make it clear in an offer letter if the role is subject to any conditions, such as obtaining satisfactory references or checking the individual’s qualifications.

- Don’t leave it too long to get your new employee to sign their contract. Ideally, you should ask them to do this before they start their new role but if this isn’t possible, ask them to sign their contract during their first week.

Employment contracts

For examples of these documents, please follow the links below:

- Statement of terms and conditions template from HMRC

- Employment contract templates offered by LawBite

At the very least, you should give anyone you employ for at least one month a statement of specified terms and conditions relating to their employment. However, you may wish to consider providing a contract of employment instead. This is a more robust document that contains additional information for the employee and provides a greater level of protection for you and your business. In addition to the information included in the statement of terms and conditions, the contract could also cover topics such as confidentiality and intellectual property.

For further employment law guidance and support, you may wish to enlist the help of an HR consultant or an employment law expert.

Employment law information provided by Louise Paull, LawBite Employment Law Brief

Paying your staff

An introduction to payroll

Each time you pay your employee, you must run payroll. This involves:

- recording the employee’s total pay

- calculating how much tax and employee’s National Insurance you’ll have to deduct from the employee’s wages and then pay to HMRC

- calculating any other sums you might need to deduct from the employee’s pay, such as student loan repayments or money that a court has ordered to be deducted, such as overdue council tax

- calculating the employer’s National Insurance contribution that you’ll need to pay

- producing payslips

- electronically reporting the employee’s pay and deductions to HMRC in a Full Payment Submission (FPS) through the Real Time Information (RTI) system

We strongly advise that you use payroll software to handle your payroll, as the calculations for tax, National Insurance and student loans in particular can get very complicated. Don’t forget that we’ve built a fully integrated payroll system into FreeAgent!

PAYE and tax codes

The tax you deduct from your staff’s wages is called Income Tax, and it’s worked out using a system called Pay As You Earn (PAYE). The amount of tax you deduct under PAYE depends on the employee’s tax code. You must enter the tax code that HMRC gives you for the employee into your payroll software.

Alternatively, if your new employee had a previous job, they’ll give you a form P45 which will display the tax code you should use. If the employee joins you part-way through a tax year, the P45 will also show how much money the employee has earned so far that year and how much tax their previous employer deducted from their wages. You’ll need to enter these figures into your payroll software to make sure you deduct the right amount of tax from your employee’s wages for the rest of the tax year.

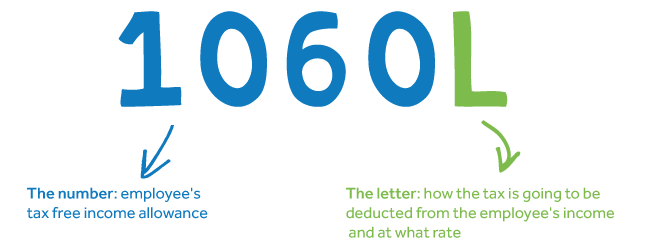

The anatomy of a tax code

The number represents the employee's tax-free income allowance (it's usually 1/10 of the total income they can earn before being taxed).

The letter represents how the tax is going to be deducted from the employee's income and at what rate. This is dictated by the employee's individual circumstances.

Employee’s National Insurance

Along with the income tax deducted under PAYE, you must also deduct employee’s National Insurance from your staff’s wages and pay it to HMRC. The class of insurance that employees pay depends on their employment status and how much they earn, as well as whether they have any gaps in their National Insurance record.

| National Insurance class | Who pays |

|---|---|

| Class 1 | Employees earning more than £242 a week and under State Pension age - these contributions are automatically deducted by employers |

| Class 1A or 1B | Employers pay these directly on their employee’s expenses or benefits |

| Class 2 | Self-employed people earning profits of more than £12,570 a year. People with profits of less than £6,725 a year can choose to pay these contributions voluntarily. |

| Class 3 | Voluntary contributions - people can choose to pay these contributions to fill or avoid gaps in their National Insurance record |

| Class 4 | Self-employed people earning profits of £12,570 or more a year |

Source: HMRC

Real Time Information (RTI)

Each time you pay your employee, you have to tell HMRC how much salary you’re paying and how much tax, employee’s National Insurance and employer’s National Insurance that HMRC can expect to receive. You must report this information electronically, either before you pay your staff or on their pay day, through the RTI (Real Time Information) system.

To get set up for RTI, you need to:

- register for HMRC’s online services (if you haven’t already done so)

- log in to HMRC’s online services for PAYE

- wait for your activation code to arrive in the post

You then need to make a Full Payment Submission (FPS) every time you pay an employee. Some software providers (like FreeAgent) allow you to do this automatically through your payroll, but you can also use HMRC’s basic tools to make a Full Payment Submission directly to HMRC.

Employee expenses

Once they’ve started in their new role, your employee may use their own money to pay costs on behalf of the business (e.g. paying for a train ticket to visit a client). In most cases, you should be able to reimburse the employee directly for these expenses. If you pay them back for expenses they personally incur, you may need to report this information on a form P11D. The form P11D is also used to report any non-cash benefits you provide to an employee during the tax year. Completing a form P11D can be tricky and time-consuming, so you might want to consider asking your accountant to do this for you.

There are certain expenses, such as some cases of travel and accommodation, that you won’t be able to reimburse the employee for directly. Instead, you will have to add these expenses to the payroll and deduct tax or National Insurance (or both) from them before you pay the employee back. Your accountant will be able to give you more detailed guidance about which types of expenses you will need to process in this way. You won’t need to report these types of expenses on a form P11D.

Auto-enrolment for pensions

Automatic enrolment is a government initiative that makes it compulsory for employers to enrol staff into a workplace pension scheme if employees:

- work in the UK

- are aged between 22 and State Pension age

- earn more than £10,000 a year

The Pensions Regulator provides an online tool that offers detailed guidance on your legal duties as an employer. You just need to answer a few questions about your business.

If you use FreeAgent, find out how it supports automatic enrolment for workplace pensions.

When an employee leaves

Looking ahead to when the employee moves on from your business, there are a few things you’ll need to do to ensure that they are paid correctly and that they have the documentation they need.

When you run payroll for the employee's final period of employment, make sure that you’ve entered their leaving date and salary correctly in your payroll software before you submit the payroll to HMRC.

You also need to print a form P45 and give it to your employee before they leave. If you use our payroll, you can produce a P45 for a departing employee directly from within FreeAgent.

Taking on your first employee: the final checklist!

- Register your business as an employer with HMRC.

- Check the employee has the right to work in the UK.

- Carry out any other checks that are required for the role.

- Decide how much and how often you’ll pay your new employee.

- Familiarise yourself with the rules of salary sacrifice if you plan to offer non-cash benefits in exchange for a reduction in salary.

- Prepare either a written statement of terms and conditions or an employment contract.

- Choose your payroll software (check out FreeAgent’s built-in payroll!).

- Register for HMRC online services and activate online RTI filing.

- Establish the employee’s tax code (ask them for their P45 if appropriate).

- Use the online tool provided by the Pensions Regulator to find out what you need to do in relation to automatic enrolment for workplace pensions.

- Check to see if your business needs to sign up to the data protection register with this assessment questionnaire.

Disclaimer: The content included in this guide is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this guide. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.