Rushing to file your tax return? Avoid these common mistakes

This article was written by FreeAgent’s Content team and our Chief Accountant, Emily Coltman FCA.

When the deadline for filing tax returns is looming, it’s easy to find yourself trying to finish yours in a hurry. Here are some useful tips to help you avoid the most common mistakes people make in the rush to file before the Self Assessment deadline each year.

Mistake 1: forgetting to declare interest received on all bank accounts

The main section of your tax return must include the interest you received on all your bank accounts for the tax year in question. The only exception to this would be a bank account on which the interest is paid tax-free, such as an Individual Savings Account (ISA).

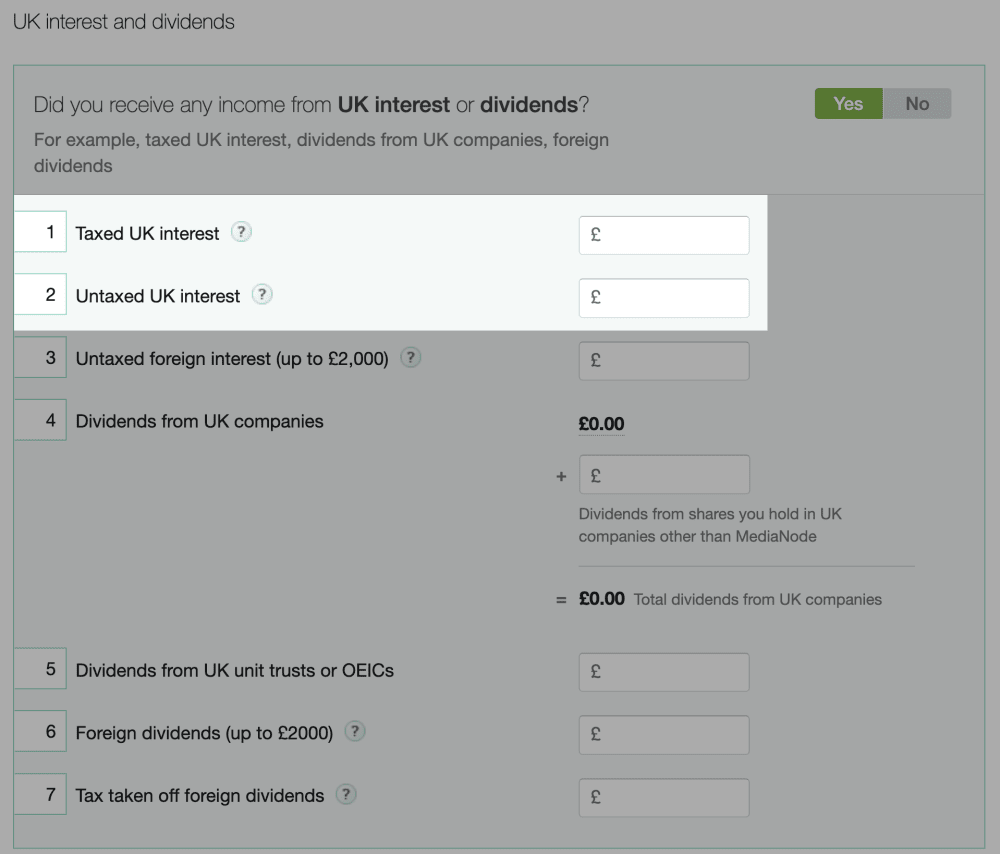

When declaring interest received on bank accounts, be sure to include:

- interest received on a business bank account

- your share of interest received on any accounts you held jointly with another person

- interest received on personal bank and building society accounts

Declaring interest received on bank accounts in FreeAgent

You can add taxed and untaxed interest to the ‘Main Return’ page of your Self Assessment tax return in your FreeAgent account.

If you’re a sole trader or a limited company director, FreeAgent’s accounting software calculates your Self Assessment tax bill from the invoices, expenses and other accounting data you enter throughout the year.

FreeAgent uses this information to populate some of the information in the Self Assessment forms automatically. If you’re a sole trader, FreeAgent can complete parts of the Self Employment form for you. The software includes built-in support to help you understand the remaining information required in each of the forms.

Once you’ve added the extra details, such as interest received on bank accounts, you can file your completed Self Assessment tax return directly to HMRC from FreeAgent.

Find out more about how FreeAgent helps you file your Self Assessment tax return with confidence.

Mistake 2: forgetting to declare business income not yet received (if you’re using the accruals basis)

If you’ve opted to use the accruals basis of accounting to prepare your accounts, you must declare all income from your last accounting year in your tax return, even uninvoiced and unpaid income.

If your accounting year end falls on the same date as the tax year end, for example, you would need to declare any income for work that you’d completed by 5th April 2025, but had not yet been paid for, in your 2024/25 tax return.

Mistake 3: neglecting to record unpaid costs

If you’re using the accruals basis of accounting, you should also record all costs from your last accounting year as well, even those that were unpaid by the business at your accounting year-end date. If the end of your accounting year falls on the same date as the tax year end, for example, you would need to record any unpaid costs that were incurred by 5th April 2025 on your 2024/25 tax return.

You will need to include two types of unpaid costs:

- costs that will be paid by the business after your accounting year end date (e.g. an office telephone bill)

- costs for which cash will never leave your business bank account (e.g. business use of home expenses and the cost of mileage for business travel)

Mistake 4: not including salary, benefits and repaid expenses from your job

If you have a salaried job in addition to running your own business, you will receive a P60 form from your employer in April or May. This will show you how much you earned in wages and how much tax was deducted. You need to record this information on the Employment pages of your tax return.

If your employer provides you with any non-cash benefits (e.g. medical insurance), or reimburses you for expenses, you will also have received a P11D form which outlines these details. Be sure to record this information, in addition to your salary and tax deductions, on the Employment pages of your tax return. If the expenses that were reimbursed were all incurred for the purpose of doing your job, include these in boxes 17-20 so that you don’t pay extra tax on the money your employer reimbursed you.

Mistake 5: forgetting to declare underpaid or overpaid tax from a PAYE Notice of Coding

If you’re employed and you underpay or overpay tax as a result of a change to your PAYE tax code change, you will receive a letter called a Notice of Coding which outlines the details of the underpayment or overpayment. You will need to include this information in the Tax Adjustments section of your tax return for the relevant tax year.

It’s worth checking this because leaving out details of underpaid or overpaid tax from a PAYE Notice of Coding in your tax return can cause problems further down the line. HMRC may try to make you pay any underpayment twice: once through your tax return and once through your tax code.

If you’re looking for even more last-minute help, check out our Self Assessment guides and blogs for a variety of useful information. If you’re in any doubt about how to fill in your tax return, you can also talk to your accountant or call HMRC’s Self Assessment Helpline.

Disclaimer: The content included in this guide is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this guide. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.