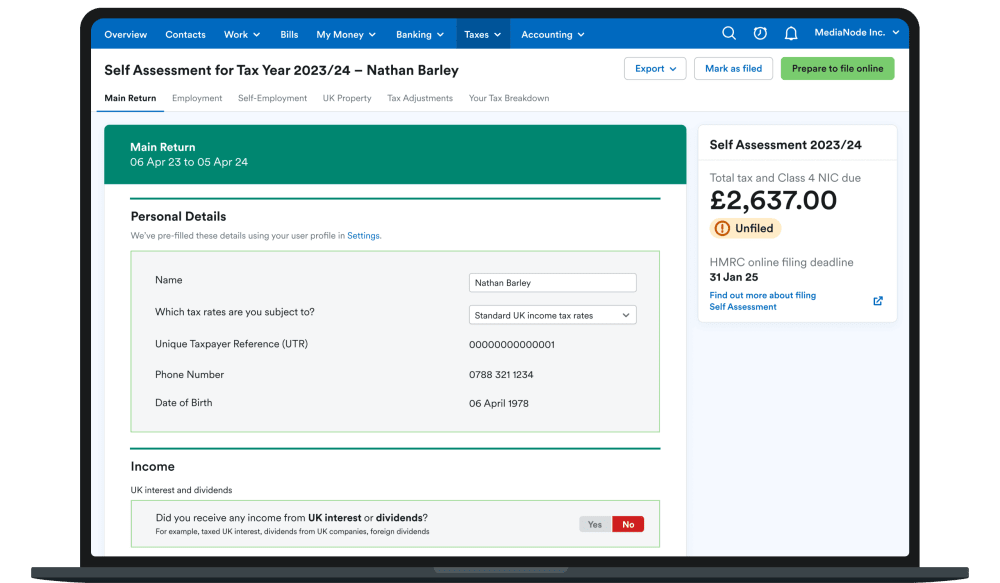

Self Assessment: what landlords need to know

If you make income from letting out a rental property, you may have to complete a Self Assessment tax return and file it with HMRC. This tax return is used to calculate any Income Tax and National Insurance you owe.

If this sounds a bit scary, don’t panic! We’re here to guide you through all the basics you need to know: when you might need to complete a tax return, what expenses you can claim for, and the records you’ll need to keep as a landlord.

And - because we know the process can be complicated - we’ve also asked our amazing Chief Accountant, Emily Coltman FCA, to answer some common questions landlords have about tax.

Before we get to that, let’s start with the basics…

When do you have to file a tax return?

If you earn less than £1,000 from property rental during a tax year, you won’t have to file a tax return because the rental would be covered by your property income allowance.

If your income from property rental for the tax year is between £1,000 and £2,500, you should contact HMRC to find out whether you have to file a tax return.

You must complete and file a Self Assessment tax return if your income from property rental is more than:

- £2,500 after allowable expenses (your ‘net profit’)

- £10,000 before allowable expenses (your ‘gross profit’)

Only ‘unincorporated’ landlords have to report property income on their own Self Assessment tax return. ‘Unincorporated’ might sound a bit technical, but it just means you own the properties as a private individual, rather than setting up a limited company to own them on your behalf. Most landlords in the UK are unincorporated.

If you haven’t previously sent a tax return to HMRC, you should register by the 5th October following the end of the tax year you’re filing for. For example, the registration deadline for the 2023/24 tax year (which ended on 5th April 2024) was 5th October 2024.

If you missed the deadline for the 2023/24 tax year, you can (and should) still register, but - be warned - you could be fined for registering late.

If you registered for Self Assessment and filed a tax return last year, you don’t need to re-register in order to submit this year’s return.

What records do you need to keep for your tax return?

In order to fill in your Self Assessment tax return easily and accurately, you should always keep a copy or record of:

- the dates when you let out your property

- your bank statements

- the rent you receive

- any income from services you provide to tenants (for example, if you charge for repairs)

- any relevant receipts and invoices for costs that you’ve incurred running the property

- any allowable expenses you intend to claim (for example, any mortgage interest)

What tax relief is available?

When filing your tax return, there is some tax relief available that you may be able to deduct when calculating your income from rental property.

Allowable expenses

As a landlord, you will be all too familiar with the day-to-day costs of running your rental property. The good news is, some of these can be deducted from your taxable income - these are your ‘allowable expenses’. Allowable expenses for landlords include:

- mortgage interest

- maintenance and repairs to your property

- water rates, council tax and utilities (such as gas and electricity)

- relevant insurance policies (such as buildings, contents and public liability insurance)

- costs of services relating to the property (such as payments to cleaners)

- letting agent and management fees

- accountant fees

- some legal fees

- rent (if you’re sub-letting), ground rent and service charges

- marketing costs (such as phone calls, stationery and advertising for new tenants)

Any expenses you claim must be wholly and exclusively related to the running of the property. The above list isn’t exhaustive, but you can find out more about what allowable expenses you can claim as a landlord in our dedicated guide.

Capital allowances

Capital allowances cannot be claimed when you buy residential properties, or when you buy furniture to put in the property, but you may be able to claim if you let a furnished holiday home or commercial property.

If you receive income from letting a furnished holiday home, you may currently be able to claim capital allowances for furniture and furnishings in the property (but not for the property itself). However, you should be aware that the furnished holiday letting tax regime is ending on 5th April 2025. If you let out a furnished holiday home, please talk to your accountant about how you should approach the end of that regime.

Any landlord may also be able to claim for equipment that’s used for the property but isn’t stored inside it. One example might include a van used to transport linen for the rental property, or large tools to make property repairs.

If you’re in any doubt about what you can claim for, you should speak to an accountant before completing your tax return. Speaking of which…

Ask an accountant: landlords’ common questions answered

To help you get as prepared as possible to file your tax return, we asked FreeAgent’s very own Chief Accountant, Emily Coltman FCA, to give you the lowdown on some of the most commonly asked questions from landlords - don’t say we’re not good to you!

Q: Should rent that’s in arrears (i.e. overdue rent that a tenant owes you) be included on a tax return?

Emily: If you’re drawing up your income on the cash basis each year - which is the default for landlords - I would suggest the arrears be included when you actually receive them. If you’re adding up your income based on when you were due to receive it (i.e. using the accruals basis) then you will need to include the arrears as at the date the tenant should have paid you.

Q: What are the tax implications of letting a property that’s jointly owned with another person, such as a spouse or partner?

Emily: You will each be taxed on your share of the property rental income, less its costs (i.e. the profit on the rental). So, for instance, if you each own half of a property that you rent out, and the rental brought in a profit of £20,000 one year, you’d each pay tax on £10,000.

Q. What are the tax implications of letting out a furnished property versus an unfurnished property?

Emily: Unless the furnished property is a holiday let (for which the special regime is coming to an end on 5th April 2025), there are no legal differences.

If you’re renting out a furnished property, or indeed if your unfurnished property contains white goods, be aware of the rules around when you can and can’t claim tax relief for replacing or upgrading furniture. In summary, you can claim tax relief for a replacement but not for an upgrade - so if you replaced a washing machine with an equivalent model, that would be allowable for tax, but if you replaced a washing machine with a washer dryer, then that would be an upgrade and therefore not allowable.

Read more about the pros and cons of letting a furnished vs an unfurnished property here.

Q: How do I claim tax relief for property maintenance and improvement costs?

Emily: You can usually claim tax relief on the costs of repairs to buildings. However, if the work results in the property being ‘significantly improved’ then that won’t qualify for tax relief.

For example, if you fix a broken window for your tenant, you could include that repair as part of your running costs for the property. It would therefore reduce your tax bill. But if you convert the attic to extra living space, that’s likely to be considered a significant improvement - and so would not qualify.

Q: What are the tax implications of using a letting agent, and how do I handle the fees and expenses?

Emily: You should report the full value of the rent (before any deductions from your agent) to HMRC. You can then record your agent’s fees and expenses as a cost (on which you can claim tax relief).

For example, let’s say you rent out a flat for £1,000 a month, the letting agent charges a fee of £100 per month and gives you £900. You need to record that as income of £1,000 and a cost of £100 - not income of £900 - to keep yourself right with HMRC.

Disclaimer: The content included in this blog post is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this blog post. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.