Frequently asked questions about P45s

As a business owner, there are lots of deadlines and documents to keep track of, not to mention a multitude of forms and returns to complete. But if your business has employees, it can get that bit more complicated, especially when managing payroll and completing forms like the P45.

To help you get up to speed with the ins and outs of the P45, we’ve answered some of the most common questions we get about P45s.

Firstly, what is a P45?

A P45 is a form that employees receive from their employer when they leave a job. A P45 shows how much tax an employee has paid on their salary so far in that tax year, as well as details of their gross earnings and their tax code.

“P45s might seem a bit challenging to interpret if you’re not familiar with payroll, but the good news is that there’s not too much to them and the format is always the same,” says Nathan Cassidy, Senior Support Accountant at FreeAgent.

When a new employee joins your business, they will need to give you a copy of their P45 from their last employer. This lets you apply the correct tax code so the employee pays the right amount to HMRC.

What does it look like?

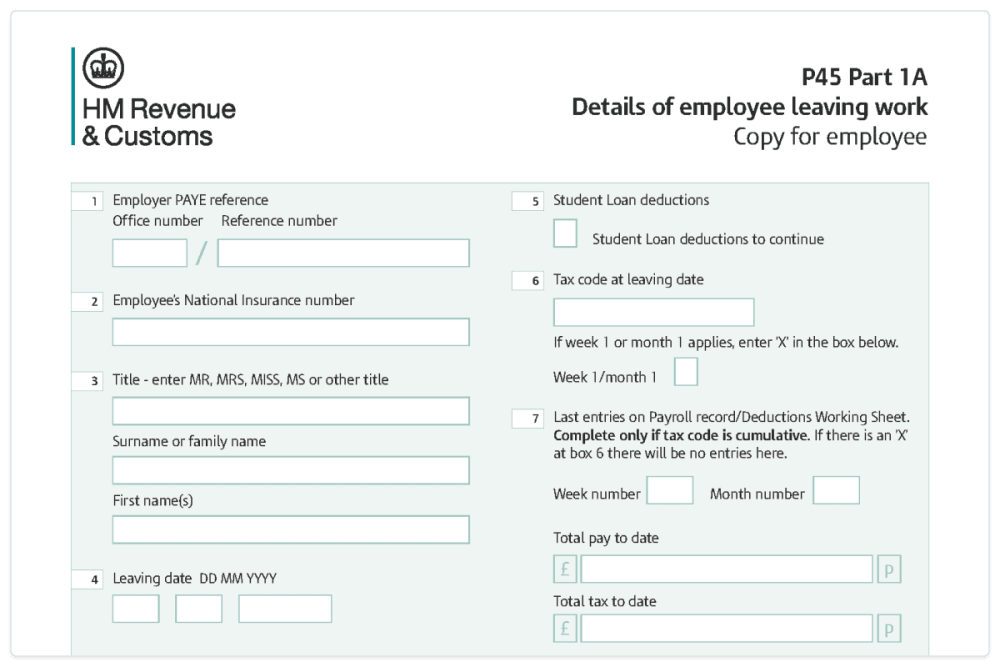

P45s are four-part documents, made up of: Part 1, Part 1A, Part 2 and Part 3. If you’re generating a P45 for a leaving employee, you must share Part 1 with HMRC and give Parts 1A, 2 and 3 to the employee. For context, this is what the top section of Part 1A looks like:

Your former employee will keep Part 1A for their own records and give Parts 2 and 3 to their new employer. It’s also recommended that employers keep a copy of any former employees’ P45s for their own records.

Got it. So, do I need a P45 if I’m self-employed?

If you’re a sole trader and you stop working, you won’t need to generate a P45 for yourself. P45s are only given to employees, and you would not be an employee of your own business if you’re a sole trader.

However, if you’ve recently become self-employed, you may need information from your last P45 to complete your first Self Assessment tax return. This will tell HMRC how much you earned from your employment in the tax year and any tax you paid through your last employer. You’ll put the information from the P45 into a set of Employment pages in your tax return. This will make sure your tax is calculated on your total income, including what you earned at your job and any profit your business has made so far.

It’s worth noting that your employment earnings may push you into a higher tax bracket. Or, if your new business makes a loss in its first year, you might be able to claim back some of the tax you paid on your salary. Speak to your accountant if you need more help with this.

If you are a limited company director and you stop taking a salary from the company, but remain as a director, you’ll need to speak to HMRC or your accountant about whether a P45 needs to be issued.

What’s the difference between a P45 and a P60?

They can be easy to mix up - both P45s and P60s show what an employee has earned and the tax they’ve paid on their salary in a tax year.

However, a P45 is only issued when an employee leaves a job, while a P60 should be issued at the end of every tax year to staff who are still working for the employer at that time. If you’re an employer, you need to provide your employees with a P60 by 31st May each year.

Still not feeling 100% confident? “Knowing when you need to issue a P45 or a P60 can be unfamiliar if you’re new to payroll, but the right software, like FreeAgent, will keep you right either way,” says Nathan.

What do I do if my new employee doesn’t have a P45?

“Having a P45 to work with makes it much easier to onboard a new employee, but sometimes they don’t have one,” explains Nathan. For example, you may hire a new member of staff who has never been employed before, or they’re taking a second job. Regardless of the reason, if a new member of staff doesn’t have a P45, you may need to ask them to complete a starter checklist for PAYE. This will provide you with the relevant starting declaration and tax code so that you can set up their payroll profile and you can avoid putting your new employee on an emergency tax code.

You can find out more about adding a new employee with no P45 to payroll in FreeAgent over on our Knowledge Base.

Heads up: it’s important to check that any new employees you hire provide a valid P45. P45s are only valid for the tax year that they refer to. If your staff member has had a break in employment, or has been self-employed for a period, and their P45 is for an earlier tax year, you may have to ask them to complete a starter checklist.

Do I have to provide employees with a P45?

Yes, when an employee leaves your business, you are legally obliged to provide them with a P45 “without unreasonable delay”. Without a P45, your former employee may be given an emergency tax code by their new employer, which could result in them paying the incorrect amount of tax.

What do I do if a former employee loses their P45?

If a P45 is lost, you cannot issue a new one. Instead, your former employee’s new employer will need to ask them to fill in a starter checklist so that they can complete their payroll.

Finally, how do I generate a P45 for an employee?

If you use payroll software, like FreeAgent, you may be able to automatically generate a P45 when an employee leaves your company. If your software can’t produce P45s and you have fewer than 10 employees, you may be able to use HMRC’s Basic PAYE Tools to create the form.

FreeAgent’s fully integrated, HMRC-recognised payroll software helps you effortlessly run monthly payroll at no extra cost. Find out how with a 30-day free trial.

Want to learn more about running payroll with FreeAgent?

Watch our ‘Payroll 101’ webinar recording, hosted by Nathan: Hit the books: become a payroll pro with FreeAgent.

Disclaimer: The content included in this blog post is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this blog post. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.