How to file your business’s final accounts

If you run a limited company or limited liability partnership (LLP), you’ll need to file a set of accounts for your business every year. Here’s a handy guide that explains what you need to include in these accounts, where you need to file them and how to do so.

What are final accounts?

The term ‘final accounts’ usually refers to the set of documents produced by limited companies and limited liability partnerships (LLPs) after the end of every accounting year. These are sometimes called ‘annual accounts’, ‘year-end accounts’ or ‘statutory accounts’.

Limited companies and LLPs both file a set of final accounts to Companies House. Limited companies also file a set of final accounts to HMRC along with their Company Tax Return.

Final accounts detail how the business has performed over the accounting year and show the company’s financial position at the year-end date. All limited companies and LLPs have to file these accounts, regardless of whether the business has made a profit.

A full set of accounts usually consists of:

- a balance sheet showing the value of everything the company owns, owes and is owed on the last day of the accounting year

- a profit and loss account showing the company’s sales, running costs and the profit or loss it has made over the accounting year

- a director’s report

- any required notes

Final accounts for micro-entities

A limited company is classed as a micro-entity if it meets at least two of the following conditions:

- Its turnover is no more than £632,000 (this threshold will rise to £1 million as of 6th April 2025)

- Its balance sheet total is no more than £316,000 (this threshold will rise to £500,000 as of 6th April 2025)

- It has no more than 10 employees

Micro-entities can use the FRS 105 financial reporting standard for their final accounts, which allows them to use a simpler balance sheet than large companies. They can file abridged accounts to Companies House that do not include a director’s report or profit and loss account. While large companies may have to file an auditor’s report with their final accounts, micro-entities can use an audit exemption statement.

Micro-entities may file abridged accounts to Companies House, but they must file full accounts to HMRC along with their CT600.

Where do you need to file final accounts?

Limited companies must send:

- full or abridged accounts to Companies House, depending on the company size (see above)

- full accounts to HMRC, along with the CT600 form as part of the Company Tax Return

- full accounts to all shareholders and anyone who can go to the company’s general meetings

LLPs have to file annual accounts with Companies House but they do not file Company Tax Returns to HMRC or pay Corporation Tax. Instead, LLPs complete a Partnership Tax Return and members are taxed individually on their share of the profits.

Note that sole traders and general partnerships do not file final accounts to Companies House or pay Corporation Tax. Instead, they submit annual Self Assessment tax returns to HMRC.

When do final accounts need to be filed?

A limited company or LLP must submit its first set of final accounts to Companies House 21 months after the date it was registered. From then on, they must submit final accounts within nine months of the end of each accounting year.

For limited companies, the Company Tax Return, including final accounts, must be submitted to HMRC within 12 months of the end of the accounting year to which it relates.

HMRC’s website contains more information about the deadlines for filing final accounts and Company Tax Returns, along with the penalties for late filing to Companies House and to HMRC.

How do you file final accounts?

Limited companies can file final accounts using accounting software. Most companies can also use the company accounts and tax online (CATO) service to file their accounts directly to Companies House and their Company Tax Return (CT600) to HMRC at the same time.

LLPs cannot use direct online services but they can file to Companies House through certain accounting software packages. Alternatively, they can send their annual accounts on paper directly to Companies House.

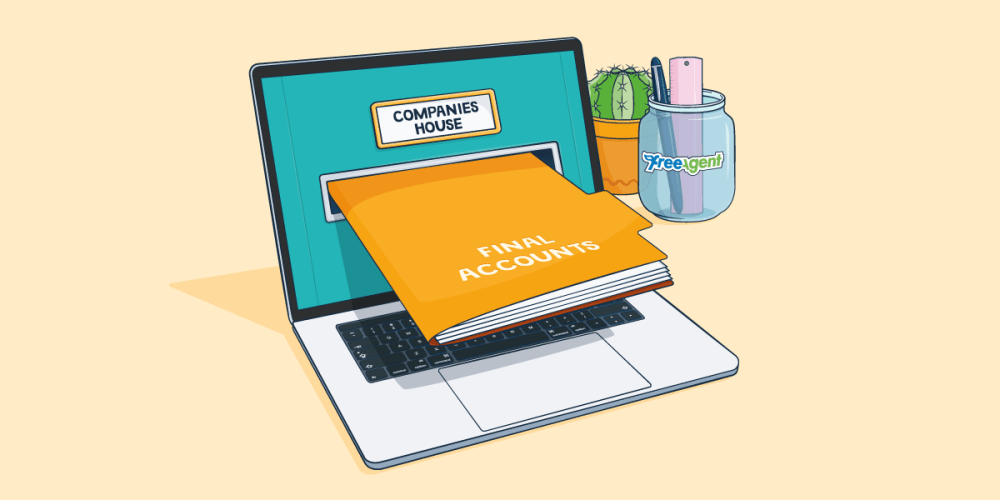

Filing final accounts using FreeAgent

FreeAgent allows many limited company micro-entities to file accounts and Corporation Tax directly to Companies House and HMRC. A ‘Final Accounts’ report is automatically generated from the data in your account and then prepared to meet the FRS 105 financial reporting standard.

Once you’ve reviewed your report, ideally with your accountant, you can file your final accounts to Companies House and your Corporation Tax (CT600) returns and CT600A supplementary pages to HMRC - all from within the software. Find out more about end-of-year filing in FreeAgent.

Disclaimer: The content included in this blog post is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this blog post. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.